One of the most long-lived of all investment newsletters, Investment Quality Trends has been making money for its subscribers since 1966, following the wonderfully old-fashioned idea that one should purchase the top dividend-paying

stocks when the dividend yield is historically high, sell when the dividend yield declines to historic lows and completely avoid stocks which pay no dividend at all.

The Lucky 13 appears in the January issue of the newsletter and shows 13 stocks we think can outperform the market.

In short, The Lucky 13 has been extremely successful and not surprisingly, quite popular. While not every stock in each Lucky 13 portfolio has been a winner, there have been sufficient winners in each group to produce 15 years of positive total returns, twelve of which have exceeded 10%.

Whether you are looking to build a portfolio from scratch, are partially invested and looking to add new positions, or are fully invested and merely in need of some affirmation and hand holding, The Timely Ten presents our top ten recommendations as of each issue.

Short of utilizing the personal investment management services of our sister company, IQ Trends Private Client Asset Management, this is as close to real time as you can get.

The Investment Outlook can be found in each issue, and is where our Editor presents his thoughts on the general state of the markets, a specific stock or industry, or a discussion about value identification and our methodology.

Since assuming the helm as Managing Editor in 2002, Kelley Wright has penned the majority of commentaries, which have ranged far and wide afield. Whether didactic, philosophical or with a touch of whimsy, Kelley most definitely has never been one at a loss for words.

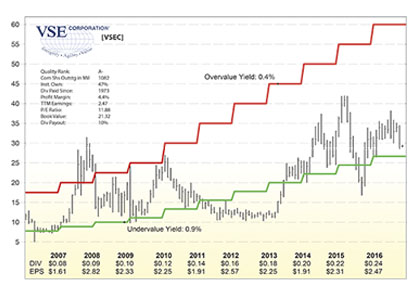

In each issue, with the exception of the first of the quarter, IQ Trends publishes four of our proprietary charts. These charts range from new entries into the Service, new entries into the Undervalued category or modified Profiles of Dividend Yield, companies in the Timely Ten, or companies that exhibit characteristics that show promise.

As a value added benefit to our subscribers, IQ Trends now allows access our archive of proprietary charts. No longer will subscribers have to wait for their favorite company to fall into one of the above mentioned categories for its chart to be published.

We love to hear from our subscribers so reach out any time. Kelley will answer your emails and calls personally. Send to subscribers@iqtrends.com.